Apple: WWDC Is Coming Bright Up. Is It Already Priced In?

AAPL is floating into WWDC on AI hope, upgrades and a familiar Cupertino glow. I first mapped the $400 path when AAPL was written off, but it was conditional: ship SenseOS, ship agency, ship proof. A prettier Siri with rented brains and “more in 2027” will not carry a mid-40s forward multiple.

AAPL has done almost exactly what I expected it might do after recovering from the Iran-war panic. Waft.

Drift higher into WWDC as shorts cover, traders chase safety in six or seven market-leading names, and Apple’s marketing department prepares to turn a new Siri glow into a product strategy.

I first set out the $400 path way back in June 2025 when Apple was being written off, even by pom-pom waver supreme, Dan Ives - but the route was always conditional.

It required execution, model choice, orchestration, and an AI layer closer to my SenseOS concept which I published before WWDC 2025, than Siri with a new hat and day-glow halo.

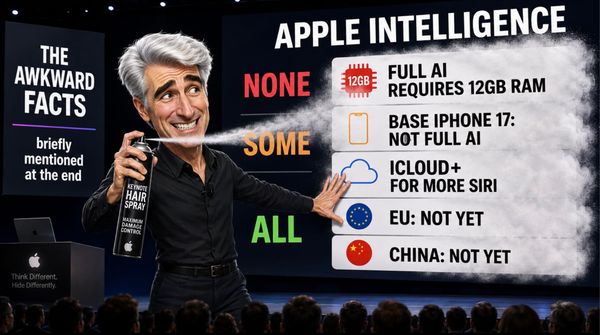

With Apple now near $310 and Wall Street warming itself around pre-keynote AI hopes, the real question is whether WWDC delivers proof, or just another beautifully lit delay, starring Tim Cook handing the reins to an ever-smiling John Ternus while Craig Federighi deploys an ozone diminishing array of hairspray products with a lit match to light a fire underneath Apple Marketing in another CGI-flaptastic display of hubris, but with another “beta“ label on everything and a promise of “more to come, soon?”

Meanwhile, here’s a quick chart screaming “OVERBOUGHT” in the short term. Disagree? Tell me why in the comments:

If you’d like to read the rest of this article, free of charge but for providing your email, just press the button and select the free tier option. You’ll receive articles direct to your inbox. Don’t worry, you can turn off this feature later, if you don’t want notification.

Note: If you are already a member, but de-subscribed from the newsletter, you will need to re-subscribe to it to access this article. Just go Account settings and re-enable the Newsletter!

I have never had much patience with the idea that AAPL should be treated as a devotional object.

This is why treating it as a trading vehicle has worked rather better than treating it as a shrine with a dividend attached and an aversion - neé detesting disdain amongst some investors, for trimming positions. As an apple farmer will tell you, you harvest when the going is good, plant when the weather and seasons are right, hunker down during bad weather and never, ever, let your orchard stand untended when you can see a clear hurricane approaching. In spite of this, the stubbornness of some buy and hold forever investors, means they often miss an obvious 50% downdraft in the making, and fail to capture the upside - which is especially important for investors who have been in the market less than 10 years and have growth targets and returns to make in the short term and can’t afford to wait 20 years until retirement.

Over the last year, each main call I have made, has been straightforward enough: buy panic when the risk/reward turns absurd, take profits when the stock returns to the usual resistance zone, and never confuse Apple’s brand gravity with a permanent suspension of arithmetic.

I called AAPL a top in March 2025 at around $240 (after selling out in December 2024 at $260), and predicted a plunge to $150-170. Three weeks later, the stock plunged to $167.

This isn’t boastful, it’s just a remark to say you can time the market, but only if you watch and understand the newsflow - including geopolitics - rather than engaging cognitive dissonance and conveniently ignoring the “disturbance in the force” you see out of the corner of your eye, but simply don’t want to acknowledge.

So after calling every rise and fall on a short term basis throughout 2025 and into 2026, I took a fresh look at the stock at the start of the Iran war.

Excuse me, should we call that a “special operation” instead? Mooted to last 3 weeks, we’re now past 12 weeks and in spite of TACOS and NACHOS there’s no end in sight yet.

When AAPL dropped towards $246 at the start of the Iran-war panic, my view was that this looked like the sort of moment where buying half a position made sense, with the rest kept back in case escalation dragged it towards $225.

If Trump performed his usual TACO routine and the market recovered, the other half could be added on confirmation rather than purchased in the middle of geopolitical fog. That is roughly how it played out. The market stopped behaving as though the end of the world was quite so conveniently scheduled, and AAPL began its familiar levitation back towards the high $200s.

When it reached the old $292 area, where I have often treated the stock as a sensible take-profits candidate, I did not call it a clean sell this time.

My read was simpler: too late to buy comfortably, too early to sell cleanly, with shorts likely covering and institutional money still hiding in the usual handful of market generals while the wider market pretended inflation, rates, tariffs and earnings pressure were details for another day. That is the kind of market which can push Apple higher even while everyone involved knows it is no longer cheap, because large-cap safety sometimes becomes the final crowded theatre before everyone remembers the exits are narrow. Anyone who has held onto AAPL running up to WWDC has two comments ready to post:

“Short sellers are ruining this because THEY DON’T UNDERSTAND!”

And the polar opposite of self-congratulatory hyperbole:

“Hah look at the stock go higher - I bet all the shorts are fleeing with their shorts burning up around their <insert nether region of your choice here>.”

I know, because over the last 25 years, I’ve been guilty of writing one or the other at least twice a year (WWDC and the inevitable iPhone - or iPod back in the day - launch. A couple of weeks ago I wondered where Apple might go and did a quick look back to 2024, and looked forward, to what 2026 might deliver:

So here we are. AAPL is around $308 today, after touching $311.80 intraday,

- with a market cap around $4.56 trillion,

- trailing EPS of $8.26, and a

- trailing P/E just under 37.5.

GuruFocus shows Apple’s forward P/E around 35.22 as of 25 May, which implies forward earnings near $8.79 at this price, while another current estimate puts forward EPS at $9.35 and the stock near 33 times forward earnings.

A move to $400 without a serious earnings upgrade would therefore imply something around 43 to 46 times forward earnings, depending on which estimate you use, and roughly 48 times trailing earnings on the current EPS base.

That is no longer a stock or investors politely waiting for proof but a full-blown buy-in with blinkers on, warranted or not, elevated by hot air and hopium.

Because Siri still hasn’t shipped and when you toss away all of the “iterative upgrades” due, the only products anyone seems to pin any growth on is .. err.. “Siri revenues” (with no attribution about how this is going to be achieved, “services,” (read financial services - ie selling on credit - and insurance sales), and absolute celebration before sight of the mythical iPhone Fold/Ultra/Whatever 9to5Mac or Mark Gurman have named it on any particular day of the week.

I was early on the $400 possibility, and I am happy to remind people of that now, partly because it irritates the right people and partly because the distinction is important.

In June 2025, when Apple had been treated as dead money and everyone was busy deciding whether the company had become a slow-motion consumer staple with better packaging, I set out the path to $400 as an execution case. It was not a prayer. It was not a farmer’s hymn or a new Book of Tommo to add to the faithful preaching “AAPL is in the clutches of short-sellers, Max Pain or buyback let-ups”.

It was a narrow road requiring Apple to rediscover shipping capacity instead ot iterating over icons, AI relevance, developer energy, and enough strategic humility to stop polishing the same delayed promises while OpenAI, Google, Perplexity, Anthropic and others kept moving past them.

As I set out in the $400 case was always conditional on execution, while the $160 case remained the mechanical consequence of multiple compression if Apple slipped into luxury-utility status.

Caption: The original scenario map before Wall Street rediscovered Apple upside.. Written on the 4th of July 2025

That framework still feels right. The difference now is that the market has moved much of the way before WWDC 2026 (almost a year after I wrote this thesis) has answered the operational question. Analysts have raised targets, with Bank of America now at $380, Melius at $385, and Wedbush already waving the $400 flag it attached to Apple’s AI potential a few weeks ago.

Amit of Evercore and Ives at Wedbush seem to have, how can I put this, a bit of a monthly circle jerk competition to see who can raise it harder and higher, quicker.

Boys will be boys, right?

This is precisely how Apple gets dangerous as a stock.

It begins with a plausible strategic path, becomes a story, turns into positioning, and then finds itself priced as though the company has already delivered the product everyone is still trying to infer from the shape of the invitation art.

It happens almost every time AAPL soars as it has done into nosebleed territory going into WWDC, with all the shorts and options plays taken off the stock in the run-up to WWDC, put back on again because with AAPL, “buy the WWDC rumour and sell the news“ is about as baked in as any stock trend could possibly be. The chances of Apple out-delivering on expectations already factored in, is low. So low, it would be dangerous to pick up the soap to pick it up with anyone else around.

That invitation art, naturally, has done its job.

Apple can make even a new shade of grey look like fashion statement after all (and they’d probably call it “Silver Fox Grey” in a deference to the age of its senior staff). Apple can make a glow around the “Dynamic Island,” otherwise known as the old compromise notch with better public relations, feel like a glimpse of consciousness from the machine.

It can take the rear camera carbuncle, rename the shelf a “Plateau,” and persuade enough people that a lump of industrial necessity has somehow become a landscape feature with intent.

“Hails the death of the Camera Bump. Long Live the Plateau!”

Apple Marketing could probably rename damp as “Ambient Hydration” and have three blogs live within the hour explaining why this changes towel ownership. The “Vapour Chamber” actually almost does just that.

The trouble is that WWDC cannot be allowed to become another exercise in naming a failure using hyperbole to distract from the unfortunate fact the new product or feature launched is less of a Hail Mary than. A bruise.

The market has seen that film.

- Vision Pro was spatial computing until it became a headset with a customer problem.

- Apple Intelligence was the future of personal AI until Siri had to go away and think about what it had done.

- The car was a 10 year project - until it was shut down, which some AAPL faithful still call a failure which doesn’t exist, because it was never actually announced.

- The F1 film was storytelling premium with Dolby Atmos, while the actual business still needed earnings acceleration and a reason for investors to believe Apple was doing more than selling belief back to people who already owned the stock.

- And Liquid Glass proved about as popular as cold sick. And perhaps, a great allegory to the Microsoft 2006 disaster of Windows Vista, a product so reviled it led to the public humiliation of the company, a desperate attempt at a comeback, which ultimately failed - exactly as the iPod gave way to the iPhone and Microsoft then spent a decade in the wilderness until rediscovering itself

As I argued here a couple of weeks ago on 14th May 2026:

Caption: The immediate predecessor on faith, valuation, and pre-WWDC theatre cycles.

Apple’s current market narrative is no longer merely about products, because faith itself has become part of the valuation machinery.

The good news, and it deserves to be treated seriously, is this:

Apple may finally be moving towards the architecture I argued for last year.

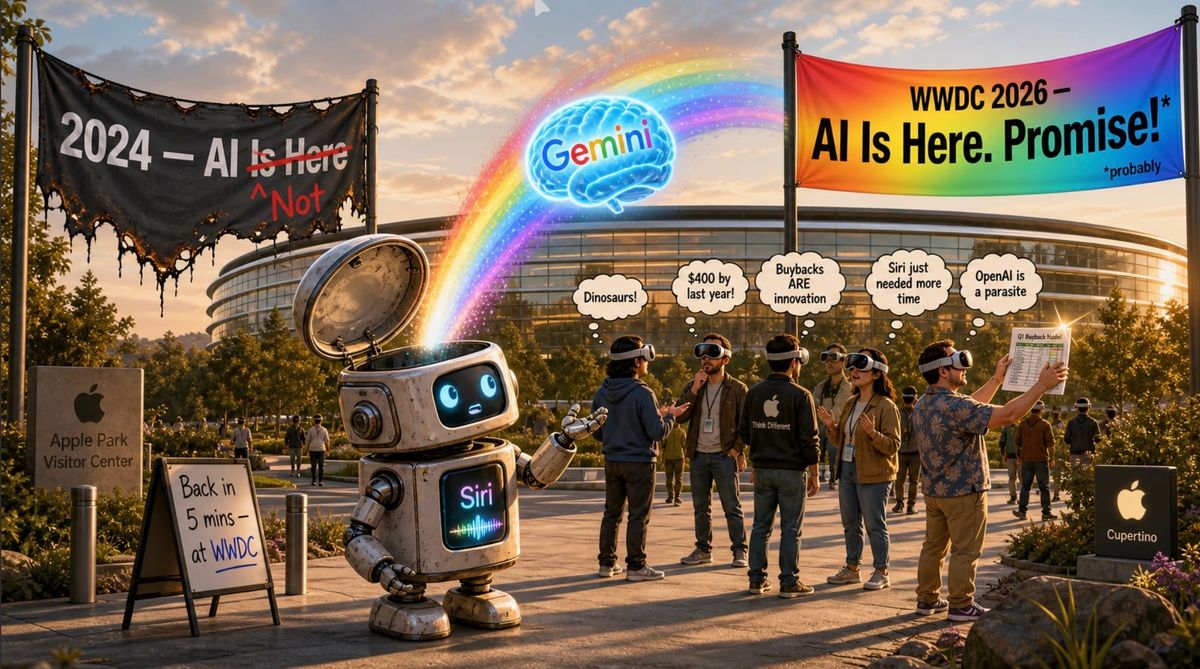

- Reports now suggest that Apple may allow users to choose third-party AI models through an Extensions-style system across iOS 27, iPadOS 27 and macOS 27, with Google’s Gemini, Anthropic’s Claude and OpenAI’s models all part of the broader rumour stream around WWDC.

- Apple may also lean on Gemini to power the new Siri, which is both practically sensible and historically embarrassing, given the company bought Siri in 2010 and then spent 15 years turning a possible interface revolution into a kitchen timer with weather issues.

This is where my June through August 2025 article, that Apple should have acquired Perplexity and my June 2025 SenseOS concept become more than archive furniture.

SenseOS was my shorthand for what Apple needed to build:

- A layer between apps, models, permissions, devices, memory and intent, capable of routing user need towards action rather than producing a prettier reply card.

- Perplexity mattered because it showed the shape of the missing thing. It was model-agnostic, citation-aware, intent-driven, and already capable of orchestrating across different model backends while presenting a clean interface to the user.

- That was why I argued Apple should buy it, harden it, integrate it, and ship it last September to time with the iPhone 17 release, leapfrog all of its competition and if they did this, I argued, I predicted - and showed how - AAPL could hit $400 by Q1 2027 rather than spend another year deciding whether humility was compatible with brushed aluminium.

Sadly Apple chose to do nothing, stick to trying to design Siri as an “answering machine,” and then abandoned that project when, well, the head of the project left Apple after a better offer elsewhere and a frustration with being unable to get Apple’s AI engineering team to produce anything he could work with, let alone stay put themselves without leaving.

October 2025 - Apple loses it’s “Siri Answering Machine” project

.. and shortly thereafter, it became apparent Apple gave up finally, after 15 years of trying to make Siri work, and two years of trying to get “Apple Intelligence” to work - and decided to rent its AI brains from Google instead.

As I wrote about the relevance of Perplexity and how Apple under Cook had forgotten the need to ship anything instead of just talking about it in internal memos, Perplexity was not the finished religion, but it looked remarkably like the working scaffolding for Apple’s missing AI layer.

Real Artists Ship, said Steve Jobs to his Macintosh team in 1984 when he discovered launch delays were due to designers fussing over their desktop icons. Literally. I also examined a possible Perplexity acquisition case as Apple’s missing orchestration layer then, which it is still missing today.

The relevant archive point is quite precise:

Perplexity was framed by me as a working prototype of the SenseOS logic and concept I outlined:

SenseOS - my concept of the agentic and orchestration layer Apple could have and should have shipped by June 2025, and still seems to be in the planning stage in 2026

A model-agnostic routing and orchestration system Apple could drop into FMF while its own models cooked, giving Siri purpose and the device mesh something intelligent to do.

Another version of the same argument put it more bluntly: FMF and Apple’s own AI could supply the engine later, while Perplexity acted as a drop-in nervous system that worked immediately.

If Apple now permits users to select models and route different tasks through different intelligence providers, it has walked onto the same road a year later, that I wrote up and extrapolated outcomes from.

I am happy to say that, because accuracy should not suddenly become impolite just because the company finally read the map after circling the roundabout twice.

Apple appears to be accepting that the future of AI on its devices cannot be a single sealed Apple brain, especially when that brain has not yet proved it can tie its own shoes in public and has been missing in action for 16 years since Appple acquired Siri in 2010, before lobotomising it.

The question is whether this becomes SenseOS in substance, or Siri with a glow-up and a rented Gemini engine behind the curtain.

Let’s get this straight:

- A chatbot does not solve Apple’s AI problem.

- A model picker does not solve Apple’s AI problem.

- A beta label does not solve Apple’s AI problem, even if it gives the legal department somewhere comfortable to sit.

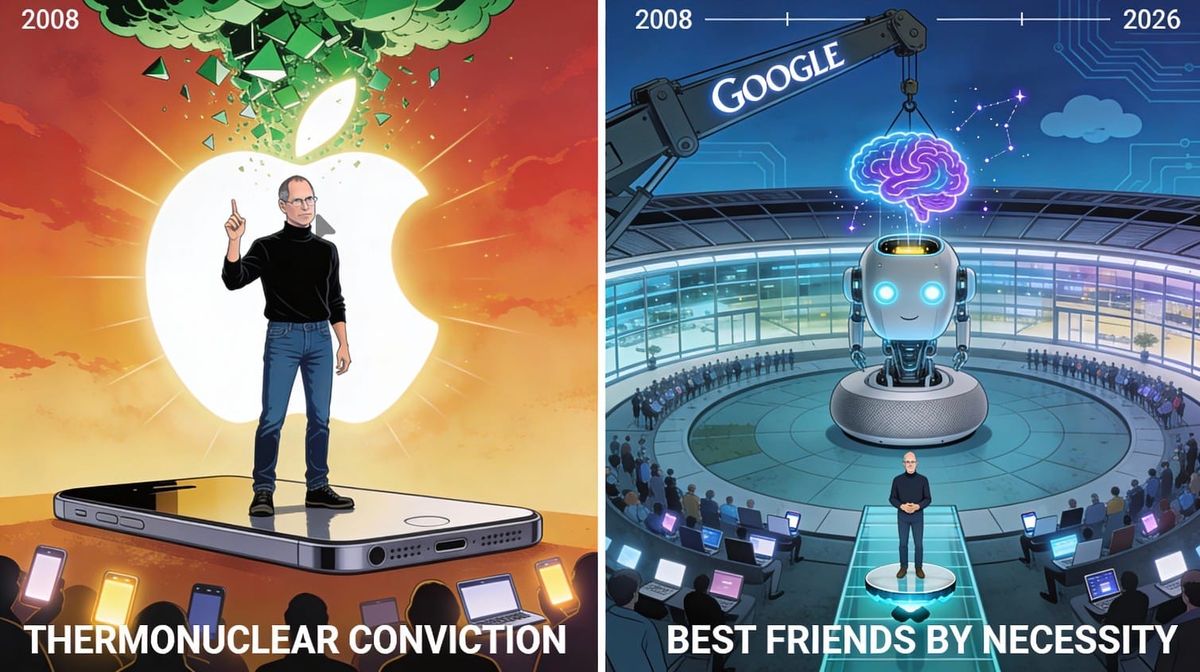

The serious test is whether Siri can understand user intent, act across apps, preserve useful context with permission, route tasks to appropriate models, give developers real hooks, and produce reliable outcomes without turning each interaction into a privacy pamphlet with animation. If they deliver that at WWDC 2026 then I’ll applaud quietly, but still hang my head in sorrow that to do it, they had to rent Google’s Gemini to do it and surrendered its own core competency in a way Steve Jobs would have self immolated at, given he declared thermonuclear war on Google for copying the iPhone with Android.

Steve Jobs protected Apple by ensuring it remained self sufficient and competent. Tim Cook et all gave up and sold Siri’s empty skull to Google to squat in, and is paying it a few Billion Dollars a year for the privilege. “Shame on you.”

For WWDC 2026, this is precisely where Apple’s instincts may still betray it.

Reports suggesting the new Siri may “forget” conversations for privacy reasons will reassure a certain class of Apple commentator over 50, who still thinks memory is creepy until their own assistant cannot remember what they were just doing.

For younger buyers like Gen-Z, it’s just going to piss them off.

Privacy remains important, but privacy without usefulness becomes a museum label. A fossil showing what was, and what dies before it could evolve.

Apple cannot spend another year telling users that a deliberately forgetful assistant is a feature because Cupertino has discovered moral purity in amnesia.

The best version of this WWDC is easy enough to describe.

Apple shows a real Siri with model choice, deep app control, developer-facing AI extensions, strong but usable permissioning, useful memory where the user wants it, and a proper path from Apple Intelligence branding into daily agency.

- It proves that FMF and PCC are more than acronyms dressed for keynote lighting.

- It shows that Gemini, Claude or ChatGPT can be used as external intelligence sources without making Apple look like a platform landlord renting out the brain room because its own tenant never arrived. Or rather, was lobotomised by Apple itself, and stuck in the dead end of an evolutionary source code fork which proved too poor to resuscitate once Apple finally realised chatbots and LLM were a “thing” and Apple’s own management who had ridiculed the notion that people might want to talk their Macs or iPhones was for the birds.

The mediocre version is also easy enough to imagine, and this is the one worth worrying about.

Apple shows a good demo, a glowing invocation state, a handful of app actions, a smoother Siri voice, a few model options, but a promise that the deeper integration will arrive later.

Developers clap. Blogs post screenshots. Analysts call it a turning point. The stock wafts higher for a few days because nobody wants to short a keynote, and then the market gradually realises that Apple has shipped an elegant waiting room. Again.

The worst version is the one where Apple labels the new Siri as beta, shows just enough to excite the blogs, and effectively confirms that the real product still lives somewhere in 2027.

That would be harder to forgive with the stock already near this valuation. Apple survived two years of AI delay because the brand still had enough trust in reserve. It survived a second year because markets can be sentimental when liquidity is kind and the market was on fire.

A third year would begin to look less like caution. I’d have to say it proved the cultural rot I’ve long written about, and Apple’s key “product“ it needs to fix before doing anything else.

Apple needed a new culture, I argued, not just a new CEO or a “Plateau.”

This is the point I made repeatedly in the $160/$400 framework.

Apple can earn a $400 narrative, and I was the first to argue in detail that it could, when very few people were willing to say it without sounding faintly deranged.

It can also lose the right to that narrative if WWDC produces glorious CGI theatre without a working product not called a beta. My archive’s original formulation remains the cleanest:

If Apple ships, iterates and convinces the market it is still a growth company, the $400 path becomes visible; if execution stalls, valuation gravity returns and the stock will be overpriced until it ships something which can fulfil the AI services and subscription models Evercore and Wedbush have used to justify their hyperbolic screams of “ever higher“ prices for 9 months.

The browser threat makes the timing more severe. Perplexity’s Comet (and now Perplexity Computer, which actually turns MacOS into precisely the agentic OS I described because it integrates, with permission, with your Apple apps and Mail) and OpenAI’s browser strategy point and GPT’s increasing integration with the OS, point towards an interface layer travelling above the operating system, with user memory, context, research, workflow and task automation increasingly living inside a cross-platform intelligence environment.

Apple’s risk is not simply that Safari loses share.

The risk is that the user’s actual working life moves into a layer Apple does not control, leaving iOS and macOS as polished hosts for someone else’s cognitive relationship with the customer. A bit like Apple has already been forced into doing, by putting Gemini into Siri’s brain and running it on Google’s servers because Apple can’t get their data centre farms up to speed fast enough in spite of promising to do just than a year ago.

As I argued in my article about the Agentic Os and AI Browsers the AI-native browser threatens Apple because the interface can move above the platform while still using the platform underneath.

AI browsers shifting the interface above Apple’s traditional operating system.

That is why WWDC26 is bigger than the usual software parade.

Apple is no longer being asked to show that it has AI features.

Everyone has AI features. And has done for two years now.

It is being asked to show that it can own the next interface layer rather than become the device layer beneath it.

If Siri remains a polite app launcher with a better animation, tand produces better “Genmojis” (always the kiss of death for AAPL whenever Tim Cook woud drag them up as his favourite feature during an earnings call) hen Apple has missed the point again.

However, if Siri becomes a true orchestration layer across models, apps, devices and context, then Apple may finally have found the road I described a year ago.

The long Siri history is the uncomfortable ballast beneath this piece. Apple did not discover assistants last winter. The company bought Siri in 2010 which was fully agentic, before the idea of an agentic assistant had been even understood by anyone else and before most consumers understood what an intelligent assistant could become.

Apple then allowed the product to spend more than a decade becoming less interesting than the idea it replaced. Apple Intelligence was supposed to correct that history, but instead became another reminder that Apple’s ability to name a future remains better than its recent ability to ship one on time.

As I explored in my canonical history of the purchase and fall of Siri over a decade and a half, Siri’s failure is a historical arc rather than a single embarrassing product delay.

The Benjamin Button of Assistants - how Siri became less capable every years until eventually abandoned in all but name. Siri’s fifteen-year failure from promise to delayed Apple Intelligence today.

There is also the demand-side question, which the Apple faithful still underestimate, because they’re mostly past middle aged and don’t understand Gen-Z, now 16-30, ”Think Different,” like they once did.

Gen-Z is not waiting reverently for Apple to decide which future is safe enough to release. They’re price conscious and fussy and are becoming increasingly disillusioned with carrying phablets in their pockets and want the notifications to just stop. If you’re a parent, have you ever managed to get your child to answer a phone call these days, let alone message you back?

Younger users already move between platforms, tools, AI assistants, music services, browsers, cloud systems and creative workflows with much less emotional attachment to the old Apple ecosystem story. They care about utility, cost, openness, agency and whether the thing works where they are, rather than whether it can be blessed inside Apple’s garden first.

In my article about Gen-Z last year, I noted that the next generation is far less interested in Apple’s inherited lock-in theology than older shareholders imagine.

Gen Z as the demand shock Apple keeps underestimating badly.

That generational shift is one reason the “installed base” argument tritely rolled out by Apple luminaries such as the esteemed Horace Dediu has become too lazy for serious use. Much of AAPL’s future rise was also predicted by the faithfull on never-ending buybacks (while I argued Apple should stop buying its own stock back with its spare cash, and start rate re-investing on a large scale in R&D). Oddly, now that Apple have made a statement they intend to do this, the same people who were lauding buy-backs as the ultimate AAPL-underpinning are now saying it’s a great thing buybacks are being slowed down, and maybe the company should invest more in R&D. Really people, sell ice to the Eskimos.

An installed base is a runway, not a guarantee. It tells Apple where the users are, not whether Apple still owns the relationship that matters. That older “installed base” are unlikely to be spending more on services, or buy financial products or insurance because they’re purchased alongside that of a new product, and with each generation the installed base ages, the less useful they are to include in “new services sales.”

Especially with Apple services general being permitted to be used by five independent friends & family members, the “hand me down“ notion that old devices will generate new services revenue is patently absurd.

A person can own an iPhone, use Spotify, browse through an AI-native browser, store work in Google Docs, treat ChatGPT as a working memory layer, and regard iCloud as an occasional nuisance with a better icon. The device may remain Apple’s but, the interface may not.

This brings us back to valuation. AAPL at $400 today would be asking investors to tolerate a forward multiple in the mid-40s before the earnings acceleration has turned up.

That is possible for a company which has clearly re-entered a growth phase, owns a new interface layer, monetises developer access, drives services higher, and turns AI into a genuine upgrade and retention engine but it is much harder to justify if Apple merely displays a more charming Siri, borrows Gemini, and asks everyone to return in 2027 for the part where the assistant becomes properly useful and the much rumoured iPhone 18 has launched along with the fold. Or is it the Ultra. Or, is the 18 delayed, so the Fold/Ultra can ship first? Nobody knows, but apparently it doesn’t matter at all.

Such is the intellectual premise behind AAPL discussion these days, especially amongst long term investors who have as much personal interest in Siri, or a chatbot or a foldable iPhone as they do in wearing a tight pair of Speedos on the beach.

The current market does not seem in the mood for such distinctions.

It is being pulled higher by a narrow group of large stocks, while inflation has not politely vanished, rate cuts remain unhelpfully theoretical, and the macro backdrop still contains plenty of sharp edges. Then there’s the tail wagging from the Hormuz fiasco, yet to hit the world big time.

Apple benefits from that because it is one of the few names big enough to absorb institutional money when managers want to look prudent while still chasing performance but this can continue into WWDC. It may also reverse quickly if the keynote reveals that the market has been buying the trailer rather than the film, and the film disappoints, as anyone who has seen the new Star Wars film - a castrated and unworthy production of the name, from. Disney, released this week.

So the line going into WWDC is not bearish. But it should be disciplined.

Apple may finally be moving in the right direction. It may finally be preparing to open the AI layer, embrace model choice, and build something closer to SenseOS than the old Siri command parser.

It may even surprise us with a product that feels less like an apology and more like a beginning and if so, the $400 path I painted in June 2025 remains alive, and the stock may deserve the benefit of a higher multiple as earnings expectations catch up. But at over $300 already, this is not a slam dunk with a 40+ fPE in the making.

If Apple arrives with a polished chatbot, a glowing island, a few careful demos, a “more later” timetable and a privacy explanation for why the assistant cannot remember enough to be useful, then investors need to stop pretending the valuation problem has solved itself.

- A Dynamic Island spectacle will not generate earnings.

- A Plateau will not rescue Siri.

- A new grey will not turn a mid-40s forward multiple into arithmetic.

Apple does not need another perfect keynote. It needs to ship the thing worthy of the price already being placed on it.

Live long and prosper and retire on your dividends, if you’re lucky. Otherwise, hold on and hang on tight because the smell of hopium is strong and so far, the hallucinations seem to be coming more from analysts stoking up investor excitement and not from any fundamental change. Yet.

See you on the other side of WWDC.

Tommo_UK, London, Tuesday, 26th May 2026

© 2026 Tommo_UK / tommo.fyi

CONTACTING ME

💡 Reach out to me using the Confidential Drop Box form below.

CONTACT ME DIRECTLY: discreetly (and anonymously if you prefer)