Hormuz May Be America’s Suez: Even Apple Is Not Insulated

Hormuz is not just a Middle East story. It is a test. Can American force still turn military action into durable order at a vital chokepoint, and whether markets, allies and consumers still believe it. If it cannot, the fallout will not stop at oil, tankers or diplomats. And Apple will feel it too.

Hormuz Is America’s Suez. Here’s why

Publisher’s note: This is not an Apple article in the narrow sense.

It is an Apple article in the only sense that really matters when the world starts to wobble. Anyone who thinks geopolitics is something that happens to “other countries” has missed the point entirely. Foreigners buy iPhones. Foreigners pay for Services. Foreign consumers, foreign currencies, foreign shipping lanes and foreign energy prices all feed straight back into Apple’s growth, margins and multiple.

As a quick aside, at the end of this article is some commentary on today’s AAPL action and some thoughts on entry points, bottoming-out support and risk/reward.

As I argued in March 2025, you cannot spend years pretending Apple is a secular-growth island and then act surprised when geopolitics, energy prices and collapsing consumer confidence turn up in the numbers.

The same people who talk up AAPL as though geopolitics were background wallpaper, Dan Ives being a reliable example of the genre, are usually the first to discover, too late, that foreigners fund Apple’s growth story too, and foreigners in stressed economies stop buying expensive hardware and paying for high-margin services.

If the Strait of Hormuz hardens into the economic choke point it now threatens to become, the consequences will not stop at tankers and diplomats. They will hit sentiment, inflation, rates, consumer spending and global equity markets, and that means AAPL as surely as it means anything else. In other words, right where Apple bulls prefer not to look until after the downgrade. Macro does not sit outside Apple. It eventually walks straight through the front door.

What follows is an attempt to explain why this crisis may prove to be less a regional war than a historic test of whether American force can still be converted into durable order. Historians will already hear the echo of Suez. Some will also hear something darker in the background.

If the Strait is not restored to genuinely free and commercially normal passage, then the operation will not have succeeded in the only sense that markets, allies and shipowners will ultimately care about.

That is why this matters, and why the comparison is not rhetorical flourish but structural warning. If you’re intrigued, read on to find out why with regime change already achieved (for the worse) this conflict could be about to escalate into a world-changing geopolitical shift of tectonic proportions.

It’s not so much “all or nothing” now as, “how can this be a win,” without total capitulation by Iran? If the Straits of Hormuz are not free flowing but controlled by a foreign power, then America’s adventure will have failed, and instead empowered Iran, not deconstructed its regime, leaving the global economy on the brink of collapse, and closer to war than the Cold War ever managed.

AAPL commentary and price levels, observations and whether AAPL is a buy or not, at the end of the article.

If you’d like to read the rest of this article, free of charge but for providing your email, just press the button and select the free tier option. You’ll receive articles direct to your inbox. Don’t worry, you can turn off this feature later, if you don’t want notification.

Note: If you are already a member, but de-subscribed from the newsletter, you will need to re-subscribe to it to access this article. Just go Account settings and re-enable the Newsletter!

Onto Iran, and the Story of the Straits of Hormuz and the allegory with the Suez Crisis of 1956.

Standfirst

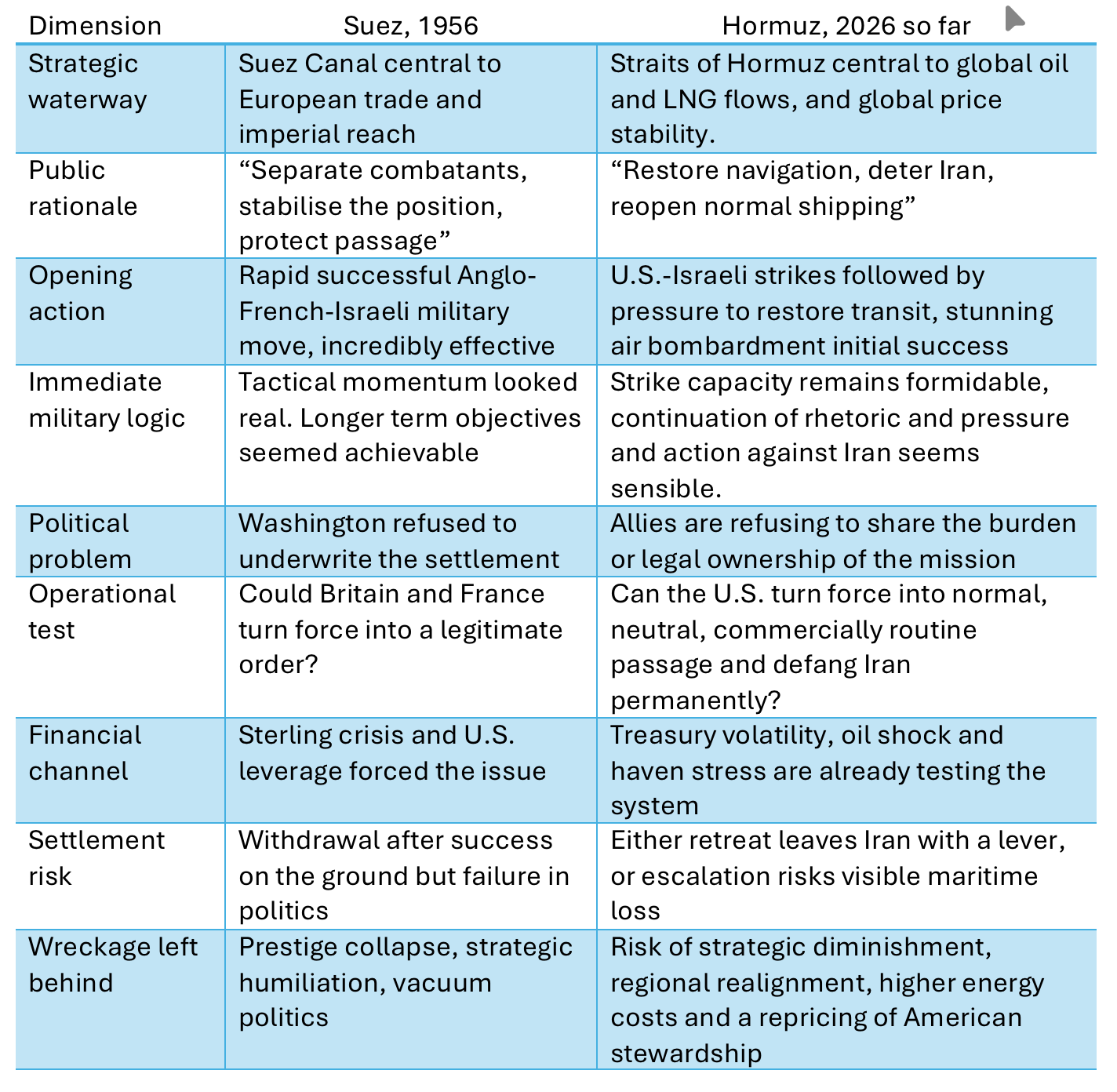

A superpower is tested not by whether it can strike, but by whether it can turn force into a durable order. Britain and France’s Suez crisis in 1956 showed what happens when military success collapses into political failure in a military adventure involving shipping lanes and regime change.

Hormuz may now be posing the same question to the United States, only with far greater consequences for energy, markets and the dollar-based system.

The Old Shelter Is Shaking

Why a rush into the dollar may be a sign of systemic weakness, not renewed faith

When systems are under strain, they rarely look broken until they break. In the past month, as the war around Iran has disrupted commercial traffic through the Strait of Hormuz and driven a broad repricing of geopolitical risk, markets have done what they almost always do in a crisis: reached for the U.S. dollar. Reuters reported on 27 March that the dollar was climbing on safe-haven demand as Middle East risks mounted, with Treasury yields edging higher at the same time. [1] That reflex is often treated as proof of American strength. It may be something colder than that. It may simply be the world running into the biggest room because the other rooms look worse.

That distinction matters because the dollar’s haven status rests on more than habit. It rests on a deep, unspoken assumption that American power still underwrites the wider system: sea-lanes remain open, Treasury markets remain the ultimate pool of collateral, and Washington, however erratic its politics, can still impose order when the plumbing of global trade is threatened. Reuters’ 26 March analysis of the Treasury market captured the fragility of that assumption rather well.

The Iran oil shock had already sent the three-month MOVE index to its highest level since the global financial crisis, widened bid-ask spreads in short-dated Treasuries, and coincided with roughly $75 billion of Treasury liquidation over four weeks. [2] A shelter can still fill up even while its beams begin to creak.

This is the paradox at the centre of Hormuz.

Money can run into the dollar and still be running away from the system that supposedly justifies that choice. That was one of the core anxieties sketched in my “Wargaming Trump’s America” in March 2025: that American unpredictability could damage allied confidence and market confidence at the same time, leaving the dollar stronger in the immediate panic yet more exposed in the longer run. [3] Hormuz now gives that anxiety a hard maritime form.

The immediate question is not whether markets can still hide in the dollar for a few days or weeks. It is whether they will continue to treat American stewardship as the least-bad anchor if a strategic chokepoint remains contested under Washington’s watch. [1][2][3]

References

[1] Reuters, “Dollar rises on safe-haven demand, yen slides as Middle East risks mount”, 27 March 2026.

[2] Reuters, “Iran oil shock sets US Treasury seismograph twitching”, 26 March 2026.

[3] Wargaming Trump’s America, March 2025.

What Suez Actually Teaches

Military success, allied rupture, financial coercion, strategic humiliation

The value of Suez is not that it gives us a slogan. It gives us a mechanism. In 1956 Britain and France acted at a maritime chokepoint, moved quickly, and achieved what looked at first like operational success. The National Army Museum’s summary is blunt: the Anglo-French intervention, launched after Israel’s move into Sinai, began well militarily but soon became a political catastrophe. [4] The U.S. State Department’s historical account says much the same thing in colder language. Britain and France, enraged by Nasser’s nationalisation of the canal and fearful for their regional standing, found themselves opposed not only by Egypt and world opinion but by the United States, which pressed hard for a ceasefire and withdrawal. [5] The lesson is not that military force failed to land a blow. It is that force failed to secure an accepted political end-state.

That point becomes clearer once you strip away the respectable language used at the time.

In the Commons on 1 November 1956, Anthony Eden framed Britain’s purpose as the urgent need to “separate these combatants and to stabilise the position”, adding that if the United Nations were willing to take over the physical task of maintaining peace, “no one would be better pleased than we.” [6]

That was the public case.

The historical record behind it is less decorous. The US State Department’s own account notes that Britain and France had entered secret consultations with Israel and that the invasion plan of Suez and Egypt was designed around an Israeli attack followed by Anglo-French intervention under the guise of separating the belligerents. [5]

Suez, in other words, was sold as order and experienced as control. That gap between declared purpose and actual design proved fatal once allies decided not to underwrite it.

It ended, crucially, not because Britain and France ran out of ships or paratroopers, but because they ran out of room.

The National Army Museum records sustained pressure on Sterling during the crisis and Washington’s refusal to support Britain financially unless a ceasefire was agreed. [4]

James Boughton’s IMF study later described Suez as a political shock that generated a financial crisis for Britain, with patterns that look strikingly modern: speculative pressure on the currency, shrinking room for manoeuvre, and international financial support turned into leverage. [7]

This is the part of Suez that modern commentary often muffles or is ignorant of. The humiliation was not only diplomatic.

It was monetary. The operation succeeded just far enough to discover that success on the ground meant little once legitimacy, alliance backing and market confidence turned against it.

That is why Suez still matters.

It was not merely the final blow and the end of an imperial era. It was the demonstration of a more durable rule:

at a chokepoint, striking is easier than settling, and settlement requires coalition, credibility and financial resilience as much as force. [4][5][7] Hormuz does not replicate Suez in costume or detail. It rhymes with it in structure. The superpower question is the same:

Can you still turn coercion into order once allies hesitate, markets twitch and the waterway itself becomes the measure of whether your power means anything at all?

References

[4] National Army Museum, “Suez Crisis”, accessed March 2026.

[5] Office of the Historian, U.S. Department of State, “The Suez Crisis, 1956”, accessed March 2026.

[6] UK Parliament, Hansard, Commons Chamber, 1 November 1956.

[7] James M. Boughton, International Monetary Fund, “Northwest of Suez: The 1956 Crisis and the IMF”, 1 December 2000.

From Tariffs to Tankers

How the fragmentation forecast in my paper last year, “Wargaming Trump’s America” has now reached the maritime phase in a crisis almost exactly 12 months on.

If Suez supplies the mechanism, the past year supplies the precondition. Before missiles, mines and escort debates turned Hormuz into a live test of American credibility, that credibility had already been spent in smaller denominations: tariffs announced as doctrine, allies treated as negotiating counterparts rather than partners, and policy delivered in bursts sharp enough to move both markets and ministries.

In Wargaming Trump’s America (March 2025) I argued that this style of power would do more than disrupt trade. It would fragment the Western alliance, accelerate Europe’s search for strategic autonomy, and turn confidence in U.S. stewardship from an inherited assumption into a variable to be priced. [8]

The April 2025 tariff shock gave that thesis a real-world rehearsal.

Reuters reported on 7 April 2025 that Jamie Dimon warned Trump’s tariff escalation could slow U.S. growth, fuel inflation and damage confidence, investment and the dollar itself. [9]

Two days later Reuters reported that the U.S. corporate bond market had effectively shut down again under tariff volatility, with spreads widening at the fastest weekly pace since the 2023 regional banking crisis and Treasury-market disruption adding to the strain. [10]

Trump then announced a 90-day partial pause on the new tariff regime on 9 April, calming markets without restoring confidence in the policy method that had rattled them in the first place. [11]

That sequence matters here because Hormuz did not arrive in a vacuum. It arrived after a year in which American unpredictability had already taught allies and investors the same lesson: policy could be abrupt, transactional and reversible, but the shock it left behind might not be.

I wrote a Tom Clancy style spoof about this, and the potential these circumstances might conspire to produce a run on the Dollar and a collapse of the bond market. You can read it here, if you’re interested in a darker and more hyperbolic narrative on “what might happen” if the US is seen to fail and Trump does a TACO one too many times, while playing with real fire and juggling knives at the same time.

A Fictional Tom Clancy spoof on a meltdown scenario in the US bond markets now seeming eerily predictive if the worst happens.

Europe’s answer was not theatrical defiance. It was institutional hedging.

On 19 May 2025 the UK and EU agreed a new Security and Defence Partnership, with explicit provision for closer co-operation on maritime security, critical infrastructure resilience, sanctions and defence-industrial collaboration, the official British text stating that it was intended in part to “help to prevent fragmentation”. [12] Less than two months later, on 10 July, London and Paris signed the Northwood Declaration, deepening nuclear co-operation and stating that there was “no extreme threat to Europe” that would not prompt a response by both nations. [13] Neither step amounted to a formal break with Washington. That would be too crude, and Europe is rarely that theatrical when money, geography and security are entangled. But taken together they signalled something more consequential: the continent was beginning to wire around American uncertainty, not merely complain about it.

Reluctance is not indifference

That caution is not the same thing as passivity. The more interesting reality is that Europe is not simply shrinking away from Hormuz. It is reconfiguring the terms on which it will act. Britain and Germany announced this month that they are moving ahead with their Deep Precision Strike missile programme under the Trinity House framework, while Britain and Norway have deepened plans to operate Type 26 frigates as a more interoperable northern fleet, tied to a broader build-up in Arctic and High North defence.

At the same time, France has been canvassing support for a future defensive maritime mission in Hormuz, and the UAE has indicated willingness to join a multinational force to reopen the strait once the shooting stops. France said on 26 March that it had approached 35 countries about a future mission to help reopen Hormuz after the fighting stops, describing the concept as a strictly defensive effort to restore maritime traffic. [50]

A day later Reuters reported that the UAE was willing to join a multinational force to reopen the strait, even as many U.S. allies still refused immediate naval participation while the war itself continued. [51]

Britain, too, has not disappeared from the board.

It is working through planning and capability questions with European partners, and at the same time deepening continental defence co-operation in ways this article has already traced. [13][53] That is the fairer reading of the moment.

That is not an alliance system snapping cleanly in two. It is something more consequential: a western and regional coalition beginning to separate support for order from deference to Washington’s management of disorder.

That distinction was always implicit in Wargaming Trump’s America.

The prediction was never that allies would simply desert the United States in a fit of pique. It was that they would begin to build around it, hedge against it, and reserve the right to define their own legal, political and military thresholds for involvement.

Hormuz is making that prediction look less like postulation and more like architecture.

- Support for the US is no longer automatic, emotional or trust-based.

- It is conditional, defensive, post-hoc and tightly lawyered. Allies are not saying the waterway does not matter.

- They are saying that if they are to risk assets and crews in it, they will do so on terms that look like collective security rather than an American improvisation with the bill left on someone else’s desk and will not be bullied.

Hormuz is where that longer drift has turned hard and visible.

Reuters reported on 16 March that Germany, Spain and Italy had no immediate plans to send ships to help police the strait after Trump’s request for support, while Britain and Denmark were more circumspect and stressed de-escalation. [14] Eleven days later Reuters reported Trump complaining that the United States did not “have to be there for NATO”, a line that did not merely express frustration but actually underscored and reinforced the logic behind allied caution. [15]

A state asked to share risk will first ask whether the guarantor still believes in the alliance system it is invoking. That is why Hormuz should not be read as a fresh crisis bolted onto the old war-gaming thesis. It is the maritime phase of the same story.

- The tariff shock in 2025 when Trump declared financial war on the world, allies and enemies alike, exposed economic unpredictability.

- The alliance drift exposed strategic distrust. Hormuz now exposes what happens when those two conditions arrive together at the world’s most sensitive energy chokepoint.

The issue is not that America’s allies see no danger in Hormuz.

It is that they are increasingly unwilling to underwrite an American operation on trust alone, having seen and felt Trump’s whims throw their sense of security and trust into the abyss with the issuance of a single tweet on “Truth Social.”

They now want guarantees that any mission is defensive, multinational, legally framed and politically survivable. That is not a refusal to share burdens. It is a refusal to inherit someone else’s undefined endgame and geopolitical chaos.

Suez may be a lesson the US administration has forgotten about, but European powers have not, and see the risk in allowing history to repeat itself.

References

[8] Wargaming Trump’s America, March 2025.

[9] Reuters, “JPMorgan CEO Dimon warns tariffs could slow US growth, fuel inflation”, 7 April 2025.

[10] Reuters, “US corporate bond market shuts again on Trump tariffs volatility”, 9 April 2025.

[11] Reuters, “Trump announces 90-day pause on tariffs”, 9 April 2025; Reuters, “What’s in Trump’s partial tariff pause”, 9 April 2025.

[12] UK Government, “UK-EU security and defence partnership”, 19 May 2025.

[13] UK Government, “Northwood Declaration: 10 July 2025”, 10 July 2025.

[14] Reuters, “US allies rebuff Trump’s request for support in Strait of Hormuz”, 16 March 2026.

[15] Reuters, “Trump says ‘we don’t have to be there for NATO’”, 27 March 2026.

The Chokepoint Test

A hegemony can strike a region and still fail to secure the waterway that matters

The wrong measure of victory.

The temptation in any crisis like this is to count sorties, destroyed launchers and damaged depots, then call that the score. Hormuz does not work like that. The real measure is duller and far more unforgiving:

do ordinary tankers and merchant ships move through the strait tomorrow in numbers that resemble normal commerce, without needing Tehran’s permission and without the market treating every voyage as a wager?

The scale of what is at stake is not in dispute. The U.S. Energy Information Administration says around 20 million barrels per day of oil moved through the Strait of Hormuz in 2024, about one-fifth of global petroleum liquids consumption, while roughly one-fifth of global LNG trade also passed through it. [16]. America releasing a few million barrels a day from its strategic reserve is not going to make a dent in that. Nothing can.

Permission is not passage.

That is why Iran’s current formulation matters so much.

Reuters reported on 24 March that Tehran told the UN Security Council and the International Maritime Organisation that “non-hostile vessels” could transit the strait only if they co-ordinated with Iranian authorities, while U.S., Israeli and other “participants in the aggression” did not qualify for innocent or non-hostile passage. [17]

The legal style of the language should not obscure the substance.

A waterway is not meaningfully open when the coastal power reserves the right to decide who counts as harmless, who gets waved through and who does not. The IMO’s extraordinary session on 19 March made the same point from the opposite direction, condemning threats and attacks on merchant shipping, insisting that navigational rights and freedoms under international law must be respected, and calling for an internationally co-ordinated approach to safeguard civilian transit. [18] Between those two positions lies the whole crisis in miniature:

Iran is asserting administered passage; the wider system is asking for restored freedom of navigation. So far, the only way to achieve that is to put “ships in the Straits” and vulnerable to mines, sea-going suicide boats, and land based attacks from Iran and Yemen. It’s Gallipoli, but at sea.

A chokepoint run by exception is still a chokepoint.

The market has already understood this, even when political rhetoric has not. Reuters reported over the weekend that Pakistan-hosted talks with Turkey, Egypt and Saudi Arabia are considering proposals that include Suez Canal-style shipping tolls and an oil-flow management consortium, while Pakistan’s foreign minister said Iran had allowed 20 Pakistani-flagged ships through the strait. [19]

That is not the language of normal trade. It is the language of workaround, rationing and improvisation. USNI News reported on 13 March that commercial transits had on some days fallen into the single digits, against a historical average of 138 vessels in 24 hours, with Pentagon officials describing the environment as “tactically complex” and missiles, rather than mines, as the most immediate threat to shipping. [20]

The point is not merely that traffic has fallen. It is that traffic has become conditional, selective and politically legible. A chokepoint managed by exemptions remains a chokepoint, only now it comes wrapped in paperwork, and payoffs.

What success would actually look like.

Once you strip the issue down to that level, the strategic question becomes clearer and less comfortable:

- An American “win” in Hormuz cannot mean simply punishing Iran, or even suppressing part of its strike capability.

- It would have to mean restoring broadly neutral, predictable, commercially normal transit through one of the world’s most sensitive energy arteries without every shipowner having to ask whether the next voyage depends on Iranian discretion or military escort.

- Nothing in the present picture shows that outcome has yet been secured.

- Iran is still talking in the language of conditional permission. Regional mediators are already discussing toll logic rather than clean restoration. Shipping remains drastically reduced. [17][19][20]

This is where the Suez parallel sharpens.

The issue is not whether Washington can hit the region hard enough to prove it still carries a hammer. It is whether, once the blows have landed, the waterway behaves as though the hammer has actually settled the argument.

References

[16] U.S. Energy Information Administration, “Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint”, 16 June 2025; U.S. Energy Information Administration, “About one-fifth of global liquefied natural gas trade flows through the Strait of Hormuz”, 24 June 2025.

[17] Reuters, “Iran tells UN: ‘non-hostile’ ships can transit Strait of Hormuz”, 24 March 2026.

[18] International Maritime Organisation, “IMO condemns attacks on shipping, calls for safe-passage framework in Strait of Hormuz”, 19 March 2026.

[19] Reuters, “Pakistan hosts regional powers for Iran talks, with focus on Hormuz proposals”, 29 March 2026.

[20] USNI News, “Missile Attacks Define Strait of Hormuz Risks, Officials Say”, 13 March 2026.

The Safe-Haven Trap

Why “money running to the dollar” may be the last reflex of a stressed system, not proof of restored American strength

The reflex and the risk.

The instinctive market response to a geopolitical shock is to run towards the dollar. That is happening now. Reuters reported on 29 March that bond yields had surged, market volatility had buoyed the U.S. dollar, and investors had moved from expecting Federal Reserve cuts to pricing in the possibility of a slight rate rise instead. [21]

On the surface, that looks like confidence. Underneath, it may mean something more anxious:

- the market is not endorsing American stewardship so much as admitting it cannot see a cleaner refuge elsewhere.

- That is a very different proposition. A haven bought out of conviction behaves differently from a haven bought out of lack of options.

A shelter can fill up - while its foundations are being tested under the load.

The paradox is already visible in the Treasury market itself. Reuters’ 26 March analysis described a sharp deterioration in Treasury-market conditions after the Iran oil shock, with the three-month MOVE index reaching its highest level since the global financial crisis, short-dated bid-ask spreads widening by around 30%, and roughly $75 billion of Treasuries liquidated over four weeks. [2]

Yet on 18 March the U.S. Treasury’s own TIC release showed that foreign residents had increased their holdings of long-term U.S. securities in January, while Reuters reported total foreign Treasury holdings rising to $9.305 trillion, up 8% year on year. [22][23]

That is the essence of the trap: Capital is still crowding into the deepest collateral pool in the world even as the plumbing of that pool is showing strain. The system has not yet rejected the dollar. It is revealing how much has to go right for the dollar to keep being treated as unquestioned collateral.

The April 2025 rehearsal.

There is a recent precedent for how quickly that confidence can wobble.

In April 2025, when Trump’s tariff shock rattled markets and Treasury yields lurched higher, Jamie Dimon warned that tariffs could slow growth, fuel inflation and damage confidence in the dollar itself. [9]

Reuters then reported on 9 April that Trump announced a 90-day pause after days of market turmoil, with analysts openly describing the move as a response to acute financial stress and instability in the bond market. [11]

That episode did not become a full-blown currency event. It did something more useful for this argument:

- it showed that the market can force a rapid reversal when policy volatility begins to contaminate the machinery beneath the rhetoric.

- Hormuz now raises the stakes because this is not a tariff dispute that can be softened with a post and a pause.

- It is a live test of whether Washington can still guarantee order at a chokepoint the world economy depends on.

- The backup of the supply chain is already in the system and being felt in Asia. It has yet to materially hit the West, but when it does, the sight of petrol prices doubling and food prices soaring amidst inflation and the possibility of interest rate hikes shows that the bad news already existing within the supply chain, is and not might going to arrive, sometime in the near future – whatever efforts are made to reinstate full supply and fill the now-unavoidable gap in supply which will last for months, or possibly years if this mission continues for more than a few weeks.

When a safe haven stops feeling safe.

That is where the real danger lies. A run on a currency does not begin because a chart looks ugly. It begins when enough holders decide the asset they thought was the exit may itself have become the bottleneck.

- If Hormuz remains contested, if energy inflation hardens,

- if the Federal Reserve is forced tighter when markets had expected relief, and

- if Washington starts to look unable either to secure the waterway or to define a credible end-state,

then haven demand can mutate into something nastier: a rush for the exits demanded from the steward – the US Dollar and the Fed - itself. [2][21]

In “Wargaming Trump’s America“ I sketched that possibility in March 2025 – prior to the near-collapse of April 9th 2025, and the logic still holds.

The issue is not whether the dollar collapses in one operatic night. It is whether doubt about U.S. power projection, Treasury-market resilience and policy coherence begins to migrate from background murmur to portfolio instruction. Once that happens, the financial consequences do not have to be total to be historic.

A partial re-weighting away from unquestioned dollar primacy would be enough to alter the strategic position of the United States, the price of its debt, and the geometry of global power. [2][21][23]

References

[2] Reuters, “Iran oil shock sets US Treasury seismograph twitching”, 26 March 2026.

[9] Reuters, “JPMorgan CEO Dimon warns tariffs could slow US growth, fuel inflation”, 7 April 2025.

[11] Reuters, “Investors react as stocks jump on Trump’s tariff pause”, 9 April 2025; Reuters, “US stocks surge, dollar gains in dramatic relief rally as Trump pauses tariffs”, 9 April 2025.

[21] Reuters, “Stocks slide in Asia, Brent crude heads for record monthly rise”, 29 March 2026.

[22] U.S. Department of the Treasury, “Treasury International Capital Data for January”, 18 March 2026.

[23] Reuters, “Japan, UK drive rise in foreign US Treasury holdings in January, data shows”, 18 March 2026.

Why Wall Street Is Not Insulated

Unlike Vegas, “What happens in the Strait of Hormuz will not stay in the Strait of Hormuz.”

If the disruption hardens, the first casualty may not be a tanker route or even a regional military balance, but the illusion that U.S. markets can absorb almost anything without having to reprice the story underneath them. That illusion has already been fraying for months.

The danger is that this shock arrives in a market already stretched thin by its own excess. Fast money has crowded into crypto, tech and AI as though liquidity were a permanent condition rather than a temporary gift.

The same speculative energy that has pushed indices to absurd levels on the way up can reverse with ugly speed once confidence starts to thin and the headlines turn from excitement to survival.

That is why the obsession with whether “the bottom is in” already feels flimsy. Markets do not always announce a turning point neatly. More often, what looks like a floor is only a pause, a dead-cat bounce dressed up as reassurance while the larger adjustment is still working its way through positioning, credit and sentiment.

The VIX around 30 today is not a trivial afterthought. It is the market’s way of saying that calm has already gone missing, even if the commentary trade is still trying to talk itself into recovery.

Last Autumn I recommended buying the VIX as a hedge against uncertainty. That seems like a rather timely call in hindsight. I hope readers with whom I corresponded about this did put on their VIX. Trades when it was then at about 18 - this downturn, even holding AAPL, would have yielded a fantastic profit by now.

Your parents told you to “always wear protection.” Advice I followed and offered in my article in November, to buy the VIX as protection against volatiity,

A market already 10 to 20 per cent off its highs, depending on what you track and where you look, is not in the mood for complacency. It is in the mood for narrative repair, and narrative repair is not the same thing as stability. Regular readers will remember that I urged VIX protection when it was still around 16, while the usual suspects were still shouting “buy” into the highs. Dan Ives, as ever, seemed to find the top with uncanny consistency. Apple at $247 from a $280 high already looks rather less like “infinity and beyond” than the sales pitch implied.

Dan Ives was still screaming BUY EVERYTHING through Novemeber and December, even after the roller coaster was already over the top. That’s three years in a row he’s screamed BUY at the top. Everyone’s favourite sartorial saboteur has been noticeably quiet of late. If you read my take, of his “TOP TEN IDEAS FOR 2025,” he’s off to rather a bad start.

That is where the real risk sits: not in the size of the first headline move, but in the possibility that the next move is forced, disorderly and self-reinforcing.

If confidence in U.S. stewardship falters while energy prices stay elevated, bond markets wobble and the dollar’s haven status starts to look less like certainty and more like habit, the adjustment will not stop at equities. Yields can climb sharply, financing conditions can tighten fast, and what begins as a geopolitical warning can become a broader market event.

Suez offers the historical rhyme.

In 1956, military overreach became financial vulnerability with remarkable speed once markets, allies and legitimacy all turned at once. America is not Britain in 1956, but the logic is close enough to make complacency dangerous.

If Washington is seen to be asserting control without securing an end-state, and if investors begin to suspect that markets have been leaning too heavily on easy money, easy narratives and easy faith in the dollar, then the unwind could be severe.

The deeper problem is psychological before it is mechanical.

Investors have spent years being trained to buy every dip, trust every rescue and assume that any period of stress will eventually meet a policy backstop. That mindset works until it doesn’t. A real geopolitical supply shock, layered on top of already fragile valuations, does not need to trigger a crash to do serious damage. It only needs to puncture the belief that risk can be absorbed indefinitely without consequence.

So the warning is straightforward. If the Hormuz crisis keeps grinding forward, markets may not be facing a routine correction but a repricing of confidence itself.

The froth around crypto, AI and big-tech momentum can vanish much faster than the television roundtables suggest.

If the dollar, Treasury yields and equity multiples start moving together in the wrong direction, the question will no longer be whether the bottom is in. It will be whether the market had been standing on thin ice all along, and the bottom if the ice cracks is, literally, unfathomable.

How the Fuse Burns

From constrained shipping to inflation, from inflation to rates, from rates to financial stress

The first link is physical, not philosophical.

A chokepoint crisis begins with movement, or the loss of it. The Strait of Hormuz normally carries around 20 million barrels a day of oil and roughly one-fifth of global LNG trade. [16] Once those flows become conditional, slowed or partially stranded as they have been for some time now, the damage does not wait for an official declaration of shortage. It begins in freight markets, insurance costs, loading schedules and refinery planning, surging futures pricing and hits consumers with their utility bills and when they tank up their car.

Reuters reported on 29 March that the Brent oil benchmark had risen 59% over the month to $115.33 a barrel, with U.S. WTI crude up 53% too, as Iran’s grip on the strait and the widening conflict pushed markets to price a prolonged disruption rather than a passing scare. [21] The fuse starts there: not in theory, but in cargoes that do not move on time and buyers forced to pay up for the barrels and molecules still available. The US is as vulnerable to rising energy prices as the rest of the world, at the end of the day, even though it may be energy self-sufficient. On signal markets, the price is not set in Washington. It is set by a ruthless Iranian regime willing to drive the price high for its own bebefit and to see its adversaries suffer not just higher oil prices, but stagnating economies.

That hit American exports. And that includes Apple, which brings in almost 60% of its revenues from overseas, not to mention its future growth resting on developing markets which will be the hardest hit from any extended fallout.

Asia feels it first. The West follows.

The geography of dependence means the first shock lands hardest in Asia.

EIA says 84% of crude and condensate and 83% of LNG moving through Hormuz in 2024 went to Asian markets. [16] Reuters’ 27 March scenarios piece said the economic effects of the war were likely to be most severe in oil-importing regions, particularly Asia and Europe, with North Asia facing the risk of power rationing and South and Southeast Asia vulnerable to fuel shortages if disruption persisted. [24]

Reuters also reported on 23 March that Saudi Aramco had cut crude supply to Asian buyers for a second month in April, routing cargoes through Yanbu and tightening refinery operations as Hormuz disruptions bit. [25]

That is how a regional war becomes a global economic problem. Asia does not absorb the shock and keep it politely contained. It bids harder for supply, reroutes cargoes, and exports the price signal westward.

Asia is not just first in line for pain.

It is the price-discovery engine for the rest of the world.

When Asian refiners, utilities and industrial buyers start bidding harder for rerouted fuel, western cargoes are pulled east (just today, four tankers carrying diesel-refining crude to Europe were diverted due to competitive offers being made mid0journey from other buyers).

So shipping patterns distort, and Europe and America begin importing the shock through higher benchmark prices, tighter refined-product balances and rising inflation expectations.

At that point, the issue is no longer whether Hormuz is “their problem first” as Washington seems to love to phrase it.

It becomes whether the West can absorb an energy-driven inflation surge at the very moment markets had expected monetary relief.

On Sunday 29th March, Japan begged markets to price oil in Brent, not Dubai prices – Brent, although higher than US WTI, is about 30% lower than locally priced Dubai oil benchmarks. This smacks of desperation to suppress pricing and impact by trying to shift pricing to a predominantly European index, not local conditions in Asia.

Will suppliers comply?

One has to ask – why should they price their deliveries to Japan on the Brent index, when traditionally it has been priced from Dubai’s – reflecting local supply dynamics. Oil doesn’t flow from. Europe to Asia after all, but locally from the Middle East to Asia.

Then the inflation story changes shape.

Once energy prices harden, central banks lose room. The market is already beginning to say as much.

Reuters reported on 29 March that investors had swung from expecting U.S. rate cuts to pricing the possibility of a slight rise, while bond yields surged and the dollar strengthened on haven demand. [21]

In Britain, Reuters’ poll of economists published on 26 March found a sharp shift in expectations: where cuts had recently seemed plausible, a narrow majority now expected the Bank of England to hold rates at 3.75% for the rest of the year as war-driven energy prices lifted inflation forecasts.

There has even been talk of the BoE raising rates a staggering four times in 2026 (very unlikely in my opinion but the BoE’s incompetence at managing the post-Covid economy offers some insight into its ability to trip up while tying its own shoelaces). [26]

That matters because this is the point at which a shipping crisis stops being “about oil” and starts becoming about mortgages, refinancing, corporate margins and fiscal room. The longer Hormuz remains impaired, the more the shock migrates from commodity screens into the everyday price of money.

By then, the system is no longer arguing about the war. It is repricing the world.

Reuters’ 26 March report on petrochemicals showed how quickly that migration can happen. With flows through Hormuz disrupted, plastic prices had already surged to four-year highs, naphtha margins in Asia had jumped violently, and manufacturers in Asia and Europe were passing higher costs through the chain. [27] The same logic applies beyond plastics: fertiliser, food, transport, packaging, metals, power-intensive industry.

By the time the shock appears in those places, it is no longer a headline risk. It is an embedded one. That is why this section matters. The article is not predicting a melodramatic overnight collapse. It is tracing the fuse to the bomb which if it explodes, might wreck the global economy and leave economic and geopolitical fallout for years, perhaps decades to come - along with empowering China and Russia with a freedom to act they’ve not had for years.

- Constrained shipping leads to tighter supply.

- Tighter supply leads to higher prices.

- Higher prices harden inflation expectations. Higher inflation narrows central-bank flexibility.

- Tighter money then feeds back into bonds, credit, valuations and sovereign financing.

If the steward of certainty and stability instead looks uncertain while that process unfolds, the haven reflex described earlier can start to feel less like safety and more like queueing at a narrowing door.

“Pax Americana,” the force which Trump has been determined to dismantle in reality but retain the benefits from? It ceases to flatten the spikes and provide stability instead leaves a vacuum for chaos and doubt. [2][21][26][27]

References

[2] Reuters, “Iran oil shock sets US Treasury seismograph twitching”, 26 March 2026.

[16] U.S. Energy Information Administration, “Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint”, 16 June 2025; U.S. Energy Information Administration, “About one-fifth of global liquefied natural gas trade flows through the Strait of Hormuz”, 24 June 2025.

[21] Reuters, “Stocks slide in Asia, Brent crude heads for record monthly rise”, 29 March 2026.

[24] Reuters, “Oil prices to stay elevated across Iran war scenarios”, 27 March 2026.

[25] Reuters, “Saudi Aramco cuts oil supply to Asia for second month in April”, 23 March 2026.

[26] Reuters, “Bank of England to defy markets and hold rates this year, economists say: Reuters poll”, 26 March 2026.

[27] Reuters, “Iran war chokes petrochemical supply, sends plastic prices soaring”, 26 March 2026.

No Clean Exit

Why neither retreat nor escalation offers an obvious path back to stability

Retreat or declaring “victory” while there is any form of Iranian control over the Straits is not neutral. It would mark one of the most epic failures in foreign policy by the US in decades.

If Washington steps back before ordinary commercial traffic is restored on ordinary commercial terms, it does not leave a vacuum in the narrow sense. It leaves a lever in Iranian hands, and they’re reportedly demanding $2 Million per tanker to guarantee “safe passage” at the moment. A quick back of the envelope translates this to $500M/month or so for Iran. At this rate, Iran won’t need to export oil itself - it can just charge others for safe passage if their oil, and rebuilding its military and assets in the meantime. Unless that is - America is really intending to put “boots on the ground“ and invade Iran.

Gallipoli shows us the risk of underestimating a foe just because you believe you have military and technological superiority.

Reuters reported on 25 March that the White House was “tracking closely” how to get oil tankers through Hormuz, but could offer no clear timeline for when unimpeded passage might resume. [28]

The same week, Reuters reported the head of the International Maritime Organisation warning that naval escorts could not guarantee safe passage and were not a sustainable solution to keeping the waterway open. [29]

That is the first half of the trap.

- Withdrawal would not return the strait to neutrality.

- It would leave behind a new precedent: a hostile coastal power discovering that conditional passage, selective permission and repeated disruption are enough to bend the market without formally “closing” the route forever.

Escalation is not clean.

The other half of the trap is visible every time the discussion turns to convoys and escorts as though they were administrative fixes. Reuters reported on 10 March that the U.S. Navy had declined near-daily requests from the shipping industry for escorts because the risk of attack was too high, even as Trump publicly insisted the U.S. was ready to escort tankers if needed. [30]

Reuters’ 25 March analysis was blunter still: Western powers spent billions trying to secure the Red Sea and still failed to restore normal commercial use, while Hormuz is harder, Iran is more capable, and neutralising the threat could take months. [31] That is what makes this section grim rather than theatrical. Escalation is not a switch that turns order back on. It is the choice to put expensive, visible steel and military into a narrow, mined, missile-watched waterway and dare the other side to prove your guarantees hollow, while being vulnerable not just to attacks from Iran, but Yemen and other bad actors.

Is the US going to launch air strikes on Yemen, as well as Iran?

Coalition sabotage

That helps explain why allied caution is not simply timidity. It is also a response to the political terms on which support is being demanded.

Trump has spent weeks complaining that allies are not doing enough while publicly belittling the help they might provide, mocking British hesitation over whether to send minesweepers or boats and treating allied support less as a coalition asset than as a stage prop.

He went as far as calling Britain’s two world class aircraft carriers “toys” that he didn’t need, in spite of them being the most powerful warships in the Western fleets aside from the US - and although undergoing maintainance otherwise battle ready and equipped to steam into action with full airwings on-board. That is, if they’re not vulnerable to w theatre of war abandoned by the US after a last minute “deal” and told that its not a US problem any longer, to ensure free paddle through the Straits.

This seems to be precisely the rhetoric from Washington at the moment though.

The UK carriers have already conducted global missions, reportedly with more F35 stealth jets on board than any single US carrier, ever, so far. Trump seems oblivious to the harm he is inflicting on his own cause, quite aside from crumbling the pride and respect the UK and US forces have for one another just to blow-off steam it would seem. It’s a fair point to make, that it is usually the closest family members, who bear the brunt of abuse in any family and there is no closer family member to the US than the UK.

That kind of contempt is not background noise.

It actively degrades willingness to share risk.

A government asked to place ships and crews in the Strait will first ask what political end-state it is underwriting, and whether Washington itself has any settled answer beyond demanding solidarity in public while scorning it in real time. Washington so far has asked for everything, offered no assurances, and issued pithy insults and degrading commentary on the very allies it needs to complete this action successfully because unless Trump wishes to avoid a Gallipoli, let alone another Suez, he cannot consider land action and a sustained incursion into Iran even in a limited manner, without allied support.

This is the point in the argument where the cold question has to be asked plainly:

is the world ready to watch a U.S. aircraft carrier, destroyer, a minesweeper or an allied escort ship take a catastrophic hit in the Gulf and discover that one sinking can do more to reprice risk than a hundred speeches can do to calm it?

We’ve already seen Iran destroy a US base in Saudi Arabia over the weekend of 28th March and pictures of a US E-3 Sentry early warning plane worth $300M in ruins – something peculiarly lacking coverage in the medi:. An Iranian strike on Prince Sultan Air Base wounded at least 12 U.S. personnel and, according to weekend reporting and published images, destroyed an E-3 Sentry/AWACS aircraft.

The sight of a sinking US warship around the Straits would be a jaw dropping and uncomfortable truth striking home in the “homeland” although unsurprising to the rest of the world: the US may not be in control of the situation, and the outcome could have longer terms implications than just energy prices, but the overturning of the existing world order, much as the opposition to Britain and France’s Suez mission from the US was absolute, and sent Britain into an economic and political decline requiring an IMF bailout.

Washington seems to be determined to repeat the mistakes of the very history lesson it imposed on the world: that imperial might can be undermined in a swift overnight blow, as America inflicted on Britain and France, changing the world forever after.

The longer the stalemate lasts, the more the world adapts around it.

That is where the strategic damage starts to outlive the battle. Reuters reported on 26 March that India had already secured around 60 days of crude supply, expanded sourcing to more than 41 suppliers, and procured LPG from the United States, Russia and Australia in an emergency effort to cushion itself against Hormuz disruption. [32]

A day later Reuters reported that Japan’s trade ministry had asked wholesalers to shift pricing from Dubai crude to Brent, while Vietnam, Indonesia and India sought Japan’s help with shortages and Japanese energy companies considered LPG exchanges with India and Indonesia. [33]

Reuters also reported Japan loosening coal-power rules from April to reduce LNG demand and buying time for alternative supply arrangements. [34] These are not yet grand new alliances. They are emergency workarounds. But that is how new economic geographies often begin: not with summits and declarations, but with cargo swaps, benchmark shifts, emergency stock releases and mutual dependencies formed under stress.

And once the workaround becomes a system, the old leverage does not simply snap back.

This was one of the more prescient instincts in Wargaming Trump’s America in March 2025: when U.S. reliability is questioned, regions do not simply wait in suspended animation for Washington to recover its nerve. They begin hedging laterally. Australia becomes more important as an LNG backstop to Asia; Asian states begin co-operating more pragmatically over refined products, stockpiles and benchmark pricing; importers seek resilience through diversification rather than deference. [8]

Reuters’ 24 March report on Santos’ temporary shutdown of Darwin LNG (Australia) is a useful reminder that these substitute routes are fragile too, which is precisely why their political significance grows when they do work. [35]

If the crisis ends badly for Washington, the most enduring consequence may not be a single military embarrassment. It may be that a region forced to improvise under pressure discovers it can do more for itself, with each other, than it had assumed when American protection still looked automatic.

Once supply chains, pricing habits and crisis diplomacy begin to rewire on that basis, the old order rarely returns in quite the same shape.

References

[28] Reuters, “US tracking closely how to get oil tankers through Strait of Hormuz, White House says”, 25 March 2026.

[29] Reuters, “IMO chief says escorts no guarantee of safe passage through Strait of Hormuz”, 17 March 2026.

[30] Reuters, “US Navy tells shipping industry Hormuz escorts not possible for now”, 10 March 2026.

[31] Reuters, “Western powers were unable to secure shipping in the Red Sea. Hormuz will be harder”, 25 March 2026.

[32] Reuters, “India secures 60 days of oil supply amid Hormuz disruption”, 26 March 2026.

[33] Reuters, “Japan government asks wholesalers to switch to Brent from Dubai pricing, document shows”, 27 March 2026.

[34] Reuters, “Japan to relax rules from April to boost coal-fired power amid LNG import risks”, 27 March 2026.

[35] Reuters, “Australia’s Santos temporarily shuts Darwin LNG plant amid Mideast supply squeeze”, 24 March 2026.

Who Gains From Drift

China and Russia do not need Iran to win the war to benefit; they only need America to fail the test

Not all beneficiaries look like victors.

The states that stand to gain most from a chokepoint crisis are rarely the ones firing the opening shots. They are the ones positioned to profit from drift, delay and the steady erosion of confidence in the guarantor.

That possibility was already built into Wargaming Trump’s America in March 2025: if U.S. credibility weakened, rival powers would not need to defeat Washington outright. They would only need to benefit from the fragmentation left behind. [8] Hormuz gives that idea a much harder edge, because every day the strait remains politically rationed rather than commercially normal is another day in which American power looks more expensive, more solitary and less definitive than it did before the war began.

China’s advantage is diplomatic and structural, not martial.

Beijing does not need the crisis to deepen forever. It needs the United States to look unable to restore ordinary order without extraordinary cost.

Reuters footage from 6 March showed China’s foreign ministry describing the Strait of Hormuz as an “important international corridor” and urging an immediate ceasefire to prevent wider economic damage. [36] Around the same time Reuters reported that China was in talks with Iran to secure safe passage for crude and Qatari LNG cargoes, even as the wider market remained choked. [37]

Yet Reuters also reported on 27 March that two Chinese container ships attempting to leave the Gulf turned back despite Iranian assurances of safe passage. [38]

That trio of facts captures China’s mechanism of gain rather neatly. It can present itself as the calmer, trade-minded power, test privileged channels with Tehran, and still point to the chaos around it as proof that American coercion no longer guarantees commercial order. It does not need to replace the United States as naval steward tomorrow. It only needs the world to imagine that more of its future trade security may have to be arranged through regional diplomacy, exception management and non-American bargaining.

Russia’s advantage is simpler, and in some ways cruder.

Moscow benefits when oil prices rise, when Western attention is divided and when European cohesion is forced to stretch across too many theatres at once.

Reuters reported on 26 March that Vladimir Putin had warned Russia not to squander the higher oil revenues produced by the Middle East conflict. [39] That is as close to an official admission of windfall benefit as geopolitics usually offers. Russia does not need to govern Hormuz or mediate the crisis.

It merely needs the price shock to persist long enough to widen its fiscal room and enough Western bandwidth to be consumed elsewhere that the strategic centre of gravity in Europe becomes muddier. In a crisis like this, distraction is not a side effect. It is part of the prize.

The quieter realignment may be regional.

The more interesting shift, though, may be happening below the superpower level.

Reuters reported on 13 March that ASEAN ministers, confronted with the economic impact of the Middle East war, stressed the need to “maintain stable, open and reliable regional energy supply chains and maritime trade routes,” while explicitly calling for enhanced intra-ASEAN trade and greater use of renewable energy. [40]

The following day Reuters reported Japan asking Australia to boost LNG output, with Tokyo describing Australian supply as a “lifeline of energy security” for Japan and the region. [41]

Set beside India’s emergency diversification measures and Japan’s shift away from Dubai pricing, both discussed earlier, those moves point to something more than emergency improvisation. [32][33]

They suggest the beginnings of a regional habit:

- Asian states learning to hedge laterally, s

- wap supply,

- reprice risk and

- build resilience with one another when U.S. protection looks uncertain or insufficient.

This does not amount to a tidy new bloc, still less a romantic Asian solidarity. It is more pragmatic than that. But pragmatism is how realignments often begin.

Once supply chains, energy diplomacy and crisis co-ordination start rewiring around regional need rather than inherited U.S.-centred assumptions, the leverage Washington enjoyed before the Iran action may not simply snap back into place even if the fighting subsides. That, too, was part of the foresight in Wargaming Trump’s America:

The most durable consequence of American unreliability might not be an immediate defeat, but the quiet construction of alternative patterns of co-operation that outlive the crisis that produced them. [8][40][41]

References

[8] Wargaming Trump’s America, March 2025.

[32] Reuters, “India secures 60 days of oil supply amid Hormuz disruption”, 26 March 2026.

[33] Reuters, “Japan government asks wholesalers to switch to Brent from Dubai pricing, document shows”, 27 March 2026.

[36] Reuters, “China urges Iran ceasefire as it stresses importance of Strait of Hormuz”, 6 March 2026.

[37] Reuters, “China in talks with Iran to allow safe oil and gas passage through Hormuz, sources say”, 5 March 2026.

[38] Reuters, “Chinese ships halt attempt to exit Hormuz despite Iran safe passage assurances”, 27 March 2026.

[39] Reuters, “Putin says Russia must take care not to squander its higher oil revenues”, 26 March 2026.

[40] Reuters, “ASEAN ministers urge halt to Middle East war as crisis rattles energy and trade”, 13 March 2026.

[41] Reuters, “Japan industry ministry asks Australia to boost LNG output amid Iran crisis”, 14 March 2026.

Wrap-up: Hormuz Is America’s Suez

A final warning about force, order, and the cost of failing to secure the waterway

There are moments in history when a great power discovers that its arsenal and its authority have quietly parted company. Suez in 1956 was one of those moments. Britain and France were still capable of striking hard, landing troops and moving quickly. What they could no longer do was define the settlement that followed, because legitimacy, allied backing and financial resilience had all begun to slip out from under them.In fact, the US sabotaged the Suez adventure by condemning it at the UN and calling the expedition reckless. In doing so, Britain and France lost their world power status and were forced into a humiliating retreat [42][43][44].

Hormuz may yet prove to be the American version of that discovery:

not a proof that the United States has become too weak to act, but a demonstration that military force on its own no longer guarantees an accepted order at the waterway that matters and that it does not possess the ability to impose a conclusive follow through with confidence.

What makes the analogy more dangerous is scale.

Suez sat astride imperial prestige and commercial traffic. Hormuz sits astride a fifth of the world’s oil and LNG, a dollar-based trading system already loaded with debt, and an alliance structure visibly less willing - in fact utterly resistant - to follow Washington into danger on trust alone any longer. [45][46][47][48]

If Suez revealed the shrinking room for manoeuvre of two fading empires, Hormuz threatens to reveal the limits of a hegemony still immensely powerful but no longer automatically believed.

That is a larger and uglier proposition. The world can absorb humiliation. It finds it much harder to absorb humiliation at the mouth of the energy system.

The comparison becomes sharper when the events are placed side by side.

This is not a claim that the two crises are identical.

It is a claim that they are structurally alike in the way that matters most:

each turns a vital waterway into a test of whether force can still be translated into order once allies hesitate and markets begin to vote.

The table above is drawn from the historical Suez record, Iran’s present conditional-passage stance, current Reuters reporting on allied reluctance, and current market reporting on energy and Treasury stress. [42][43][44][45][46][47][48][49]

That is why this crisis has such a claustrophobic feel to it.

- If Iran does not lose its practical grip on the strait, the United States cannot honestly claim to have won in the only sense markets and shipowners will care about.

- But if Washington tries to impose that outcome by force, it enters the most dangerous part of the maze: mine-clearing, escorts, missiles, drone attacks, commercial hesitation, allied equivocation, and the permanent possibility that one burning hull on a live feed does more damage to the American century than a month of carefully phrased reassurance ever could.

This is where history stops being a seminar and starts being a warning flare.

Suez ended with the humiliating realisation that the operation could not be politically consolidated because of lack of international support - and American condemnation. Hormuz risks ending with something worse: the realisation that the world economy itself may now sit inside the gap between strike and settlement, and that the US is no longer supported by its hitherto-allies but has in fact seen them turn against it. [44][47][48][49]

So the verdict is this.

Suez was the moment Britain and France discovered they could still act like empires only to discover afterwards that they had ceased to command the conditions that made empire sustainable. The lost US support, financial support and politcal support. Down was left in Egypt’s hands. Unlike Egypt, Hormuz may end up in a hostile country’s hands in effect pulling the strings of the global economy. Iran need do nothing but wait and if Trump fails to follow through, then Iran wins and America loses, no matter what military victory Washington may declare.

In the absence of the collapse of the new militant and aggressive Iranian regime - now run by hardliners who make the previous regime look like cuddly Teletubbies - Iran will emerge more powerful than ever, and the entire world weaker. Trump’s legacy, in the absence of an absolute victory, could be to be an absolute loser, condemning Iran and its neighbours to the reimposition of the hardline militant Islamic regime of the last 49 years re-invigorated and seething for revenge.

It is hard to see how any “deal,” other than one which involves voluntary free passage through the Straits with peacekeepers stationed there permanently by Iran, can possibly cast as any form of win except a brief smokescreen for American withdrawal and retreat.

Hormuz may become the moment the United States discovers that it can still strike like a hegemony - while no longer being able, on its own, to settle matters like one.

If that happens, the damage will not stop at the Gulf. It will reach into:

- energy markets,

- alliance structures,

- reserve management,

- shipping law,

- regional diplomacy and

- the quiet habits of global finance.

Suez marked the end of one illusion, and ended the remnants post-World War 2 of Britain and France’s imperial ambitions and reach.

Hormuz may mark the beginning of the end of another.

- Not the collapse of American power in one theatrical night, but the point at which the world begins, in earnest, to price a life after unquestioned American stewardship. [42][44][45][48][49]

What then, for the Dollar, US debt, and US markets?

For answers, re-read my “Wargaming Trump’s America” from March 2025. If you don’t have access to it, feel free to request it (you’ll have to subscribe first). Meanwhile, perhaps if Apple can get Siri working again thanks to Google’s Gemini being installed under the hood by September (missing the intended date of May 2026 as announced by Craig Federighi last year, it might seem), perhaps Apple Intelligence might be able to offer an answer to that question.

But given Apple’s performance with intelligence, I wouldn’t bank on it.

On that last note, a brief comment about AAPL:

Closing at $246 today ($245 after-hours), AAPL is not yet either at a natural bottom or oversold. It is attractive again, longer term, now that the premature absurd from of the latter half of 2025 and Dan Ives commentary has finally worn off.

At $245, maybe it’s worth sticking a toe in for a partial positive, but I’d wait for a fall just in case of a Trump-a-pocoalpse in Hormuz - for a full position, or a complete resolution of the conflict. $I’ve pinned $225 as “fair value” for awhile, and that’s where I see the stock finding very strong support in a sell-off. $245 now though, offers a decent technical setup for entry based on the technicals and chart action for the reasons below (Although note the $238 level mentioned).

- RSI on the 1yr and 5 yr is around 35 (20 is oversold) - not oversold meant means - and the Lower Bollinger Band on the 1-year is around $244 – and trending downwards.

- On the 5-year the Lower BB sits at $238, also trending downwards.

- If the market rises then a rising tide floats all boats.

- But if the geopolitical situation worsens there’s unlikely to be any rising tide other than dead bodies off the coast of Hormuz.

I anticipate any sharp sell-off in AAPL to stop-0ut around $225, which would be my buy-in point.

If you’re feeling lucky then today’s ~$ 245 looks like a good point for a partial buy. It’s been a level I’ve called for, for awhile, but that was before Hormuz.

If you’re feeling lucky, let me know in the comments! It’s certainly a better entry point than $280 when Dan Ives was screaming “BUY” at the top of his voice.

Tommo_UK, London, Monday, 30th March 2026

© 2026 Tommo_UK / tommo.fyi

Subscribe for free by accepting early Founder Member access to this tier — and early beta access the moment it goes live.

CONTACTING ME

💡 Reach out to me using the Confidential Drop Box form below.

CONTACT ME DIRECTLY: discreetly (and anonymously if you prefer

References

[42] Office of the Historian, U.S. Department of State, “The Suez Crisis, 1956”, accessed March 2026.

[43] UK Parliament, Hansard, Commons Chamber, 3 November 1956, statement recalling the purpose of separating combatants and stabilising the position.

[44] James M. Boughton, International Monetary Fund, “Northwest of Suez: The 1956 Crisis and the IMF”, 1 December 2000.

[45] Reuters, “Pakistan hosts regional powers for Iran talks, with focus on Hormuz proposals”, 29 March 2026.

[46] Reuters, “Iran tells UN: ‘non-hostile’ ships can transit Strait of Hormuz”, 24 March 2026.

[47] Reuters, “US allies rebuff Trump’s request for support in Strait of Hormuz”, 16 March 2026.

[48] Reuters, “Stocks slide in Asia, Brent crude heads for record monthly rise”, 29 March 2026.

[49] Reuters, “Iran oil shock sets US Treasury seismograph twitching”, 26 March 2026; Reuters, “US tracking closely how to get oil tankers through Strait of Hormuz, White House says”, 25 March 2026.